Moody’s Downgrades Indonesia’s Outlook to Negative

Continue reading to find out why.

What Was the Rationale Behind The Downgrade?

Last night, Moody’s downgraded Indonesia’s credit outlook from stable to negative, although still reaffirmed their Baa2 rating.

The downgrade was largely due to growing warnings about policy uncertainty around Danantara & fiscal policy direction, and concerns over policy predictability, governance, and institutional clarity under the current administration.

Key risks stem from higher reliance on public spending; greater focus on using public spending to drive growth poses fiscal risks, particularly given Indonesia’s weak revenue base.

However, Baa2 rating is reaffirmed because of Indonesia’s resilience: ~5% GDP growth, deficits below 3% of GDP, and debt levels still below Baa peers, assuming continued policy discipline.

Rupiah Weakened, Bond Yields Spiked

When Thailand was downgraded last year by Fitch, 10Y bond yields spiked up by 50 bps immediately, and the Thai Baht depreciated by around 6%. The stock market traded sideways for the months after.

In Indonesia, the Rupiah weakened to ~16,825 against the USD on the news. 5Y bond yields went up to 5.79%, and 10Y yields spiked to 6.43%. In equities, the Jakarta Composite Index (JCI) closed out lower by -2.83% during the first trading session.

We expect some foreign selling across Indonesian Government Bonds. However, given that foreign ownership currently stands at only ~13%, we do not anticipate a huge significant impact on yields.

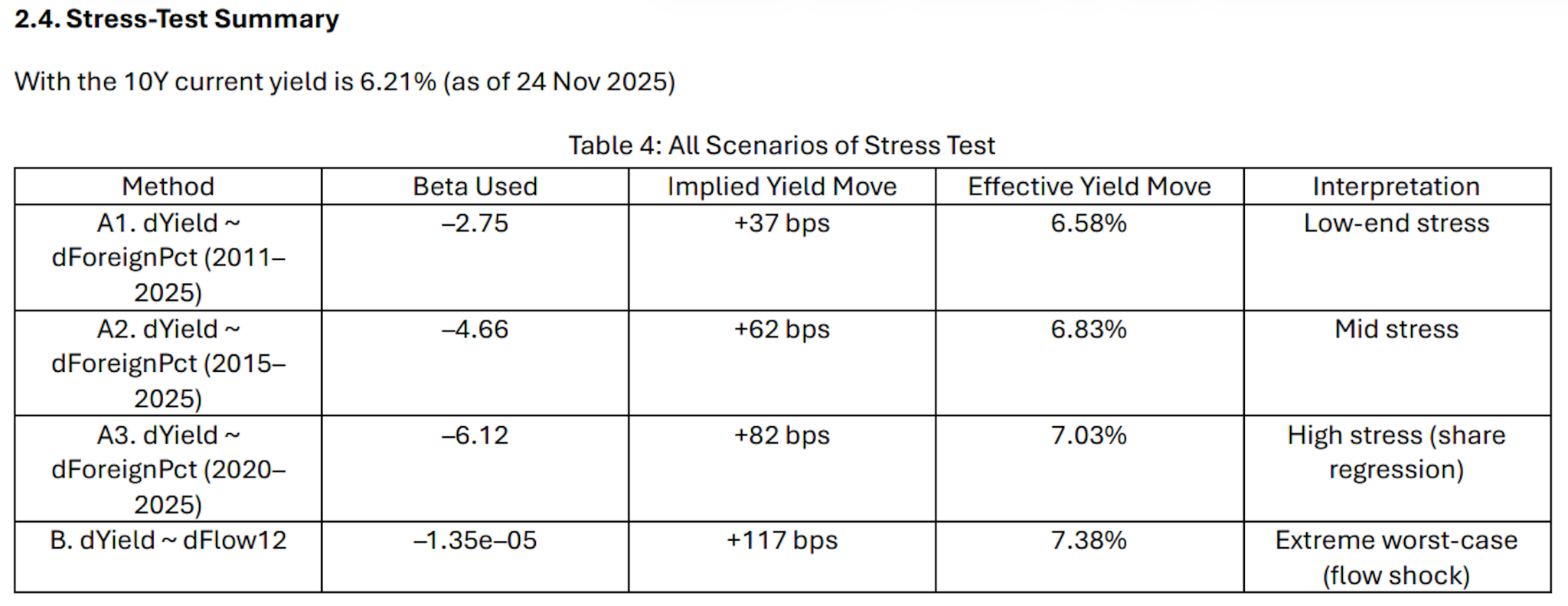

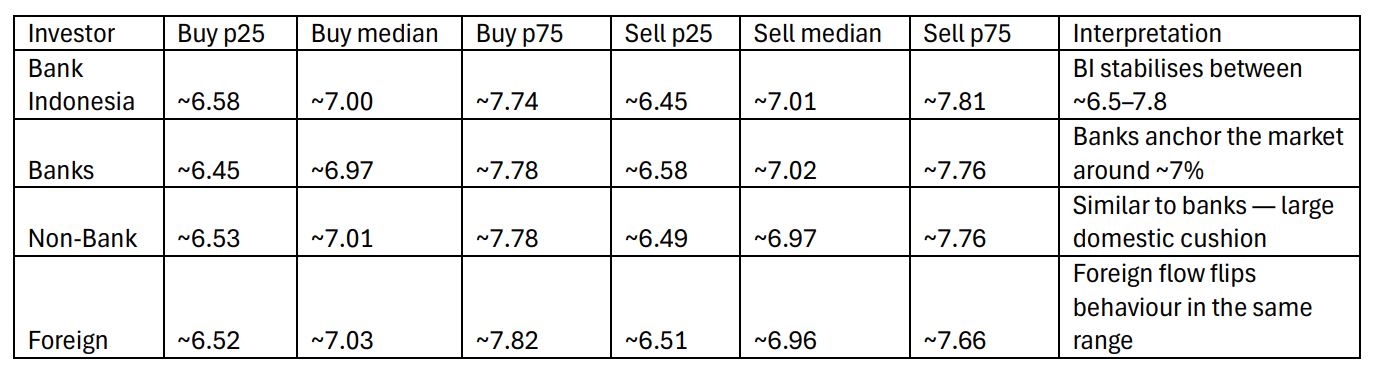

In fact, our earlier stress-test analysis shows that even in a scenario where foreign investors exit entirely, yields would move only marginally, as domestic institutions—Bank Indonesia, insurance companies, and pension funds—are likely to step in and absorb the supply.

The tables below outline the various stress-test scenarios—showing how far yields could move under foreign selling—and the yield levels at which domestic institutions typically step in to buy.

What’s The Takeaway?

As we’ve mentioned in previous articles, 10Y bond yields approaching 6.5% would signal a good entry point to begin rotating into our Bond Fund. With yields now around ~6.4%, we see a solid opportunity to start topping up gradually. That said, as the news is still very fresh, we recommend staying cautious still, as we do not know how volatile the markets would be in the coming weeks or months. Rather than buying aggressively, a phased and measured approach remains more appropriate for now.

If you’re seeking bond exposure without going fully into bonds, our Smart Cash bundled products are worth considering. They combine our Cash Fund and Bond Fund, offering a boost from government bond yields while keeping risk low and stability high.