The Bond Market Myth Everyone Still Believes

What would happen if foreign investors dump all their Indonesian Government Bonds? The short answer: not much.

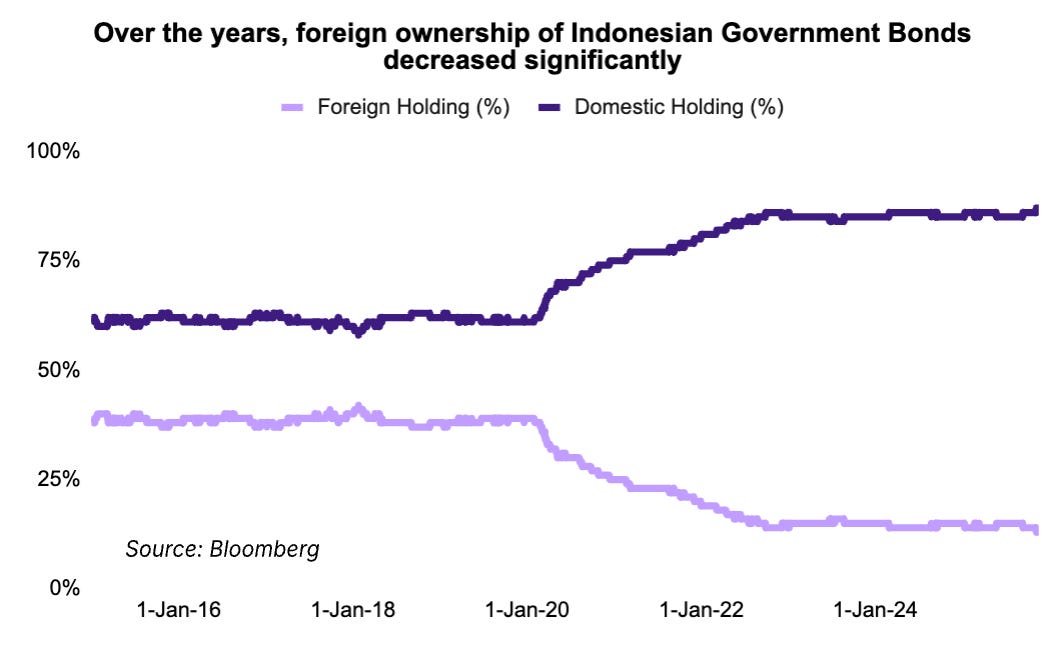

10 years ago, when foreign investors sold Indonesian Government Bonds, prices would go down and yields jumped. Today, things are different.

1. True or False: Foreign investors are still the biggest owners of Indonesia’s bond market

False.

Over the years, foreign ownership in Indonesian Government Bonds have decreased significantly. A decade ago, foreigners held almost 40% of Indonesia’s Government Bonds. Today, they own only about 14%.

In 2025, we noticed something interesting: when foreigners sold, bond yields barely moved. Sometimes, they even went down.

Why? Because most of the demand is now driven by domestic investors: banks, insurers, pension funds, and BI.

Bottom line:

Foreign flows don’t move the market the way they used to.

2. True or False: If foreigners sell all their bonds now, yields would spike

False – in real life, yields would barely move.

Let’s imagine an extreme hypothetical scenario: Foreign investors dump all their government bonds at once. What would happen in today’s real market? Almost nothing. Our Investment Team conducted a stress-test analysis and results show that yields would move only 0 – 5 bps.

*For more information about our methodologies, click here.

Why so little movement? Because domestic investors would immediately step in:

Banks have a low funding cost of ~1 – 2%. Currently, bank deposits are around 4.5% - 5.5%, so even with deposits, these banks still get quite a good spread to invest in risk-free instruments. Buying bonds yielding 6.5 – 7% is an easy profit.

Insurance companies & pension funds have structural duration mandates and always need long-term assets.

Bank Indonesia would likely step in to smooth volatility.

Bottom line:

Domestic dynamics explain why the market behaves oppositely to the foreign outflow narrative: foreign selling → domestic buying → yields stay stable or even decline.

3. True or False: If domestic do NOT absorb foreign selling, yields would soar above 7%

True, theoretically. But based on historical data, this is highly unlikely.

Let’s imagine a scenario where foreigners sell everything and domestic investors buy nothing. (This will never happen, but it shows the theoretical limits.)

In this scenario:

Yields might rise 40 – 120 bps

The 10-year yield might move from ~6.2% to 7.0 – 7.3%

But again, this is the maximum theoretical damage, not a real life scenario. In reality, domestic buyers would step in long before yields reached those levels, because who wouldn’t buy bonds when yields are that high and the cost is getting cheaper?

Bottom line:

Yields only soar if domestic investors vanish. Historically, they never have.

4. True or False: Domestic investors don’t have enough money to absorb foreign outflows

False – based on historical data, domestic investors have more than enough capacity to absorb foreign selling.

Estimated domestic buying capacity:

BI: ~IDR 250T

Banks: IDR 300 - 450T

Non-banks: IDR 300 - 900T (though not realistic due to constraints)

Total domestic capacity: ~IDR 850 - 1,600T while foreign holdings: ~IDR 868T.

Bottom line:

Even if foreigners sold everything, domestic buyers could absorb all of it, and still have extra cash.

5. True or False: When yields rise, nobody buys.

False. It’s the opposite: rising yields trigger more buying.

Different domestic buyers have natural “buy zones,” creating stability:

Banks load up at 6.45 - 7.00%

BI tends to support yields around 6.60 - 7.00 %

Insurance & pension funds love anything above mid-6%

This overlapping demand creates a yield floor: a natural anchor that keeps Indonesia’s bond market stable.

A Final Thought

Indonesia’s bond market today is deeper, more resilient, and more domestically driven than ever. Foreign flows still matter, but they no longer dictate where yields go.

Current 10Y yields are sitting around ~6.2%, supported by strong domestic demand. We think that the market structure has changed in 2025 and strong domestic demand from banks, non-banks and Bank Indonesia have supported the market. It seems Indonesia is less reliant on foreign flows but there are some risks for 2026 including a larger fiscal deficit, higher inflation due to the government’s aggressive fiscal policy, and the country’s macroeconomic risk (i.e. political and economic uncertainty).

We think that 10Y yields at 6.2% remain reasonable but not so attractive as an entry point for our investors. We prefer to see 10Y yields closer to 6.5%, offering some margin of safety, before recommending our clients to invest in Simpan’s Bond Fund.

Once 10Y yields reach closer to 6.5%, we think our Bond Fund is attractive if you’re looking for a simple way to benefit from this kind of market without tracking every yield move or policy announcement. The Bond Fund is designed to capture opportunities when yields are attractive and stay steady when the market gets noisy.