The MSCI Overhang is Largely Behind Us

May tested investor conviction. We break down the MSCI overhang, Indonesia’s market challenges, and how we are positioning portfolios through continued volatility.

May has been a month that tests conviction.

Indonesia’s capital markets have faced a confluence of pressures, some structural, some self-inflicted, and navigating them has required a clear head and a willingness to sit with discomfort a little longer than feels comfortable. If you have been watching your portfolio with one eye and the news with the other, we hope this update gives you a cleaner picture of what is actually happening, and what we are doing about it.

The MSCI review concluded with six Indonesian equities removed from the MSCI Indonesia Standard Index, effective 29 May. The outcome was sharper than we initially anticipated, likely a consequence of MSCI immediately incorporating KSEI’s disclosure of concentrated ownership structures, which reduced the recognised free float of several names overnight.

Indonesia’s weighting within the MSCI Emerging Markets Index is now expected to decline from roughly 0.72% to 0.61%, a reduction of nearly 15.3%. We estimate combined outflows from active and passive funds tied to the exclusions at around USD 1.7 billion, with total potential outflows, including the broader downweighting effect on remaining constituents, approaching USD 2.8 billion. The Jakarta Composite Index reflected this, falling as much as 4% to a low of 6,400 before partially recovering to a loss of 1.85%, closing at 6.599.24 as of 18 May 2026.

But here is the more important point: we believe the risk of Indonesia being reclassified into Frontier Markets has now been effectively removed. The remaining overhang is about index weighting, not existential market status. Much of the worst-case scenario appears priced in. That does not mean smooth sailing ahead, near-term pressure on equities is likely to persist but it does mean the character of the risk has shifted. That matters.

Indonesia’s Ongoing PR Challenge

There is a version of this update that only talks about MSCI flows and rupiah levels. But that would miss what is, ironically, the more consequential issue right now, Indonesia’s relationship with its own narrative in front of a global audience.

Recent remarks from government leaders on the rupiah’s depreciation have done little to reassure international markets. At the time of writing, the rupiah has weakened toward 16,750 against the dollar. The framing around exchange rate moves as something manageable misses a structural reality: the US dollar is deeply embedded in Indonesia’s economic engine. Imported fuel, subsidised commodities, the soybeans that go into the tempeh and tahu on your table, all of it priced in dollars. When the rupiah weakens, that cost does not stay in a spreadsheet. It filters through to businesses and households, quietly and persistently.

Beyond currency, the deeper issue is one of predictability. Global investors, whether allocating short-term portfolio flows or committing to longer-term foreign direct investment, do not just price fundamentals. They price their confidence that the rules of the game will remain consistent. When that confidence wavers, capital finds somewhere else to go. And rebuilding trust, as most investors instinctively know, always takes longer than losing it.

Where we stand, and how we are positioned.

Despite the turbulence, we believe Indonesia’s capital markets are gradually approaching a bottoming phase. We anticipate continued intervention from Bank Indonesia and the government to support rupiah stability, and with the MSCI uncertainty now largely resolved, the conditions for sentiment to normalise, slowly, unevenly, are beginning to take shape.

Here is how we are thinking about the major asset classes right now.

Fixed Income

Indonesian government bond yields are hovering around 6.8% (Indo 10Y), a level that presents a genuinely attractive entry point for investors already holding rupiah assets. We have been recommending increasing fixed income exposure and lengthening duration at current yield levels. This remains our preferred positioning for Bond Funds.

Equities

Near-term volatility is not going away, and we will not pretend otherwise. But we continue to believe that equities remain the most compelling long-term asset class for participating in Indonesia’s structural growth story, more so than dollar assets or other rupiah-denominated classes. Short-term noise, however uncomfortable, does not change that underlying calculus.

Dollar exposure

Dollar-denominated assets continue to serve as a genuine hedge and portfolio diversifier in this environment, and we may have a specific Simpan update on this front coming soon.

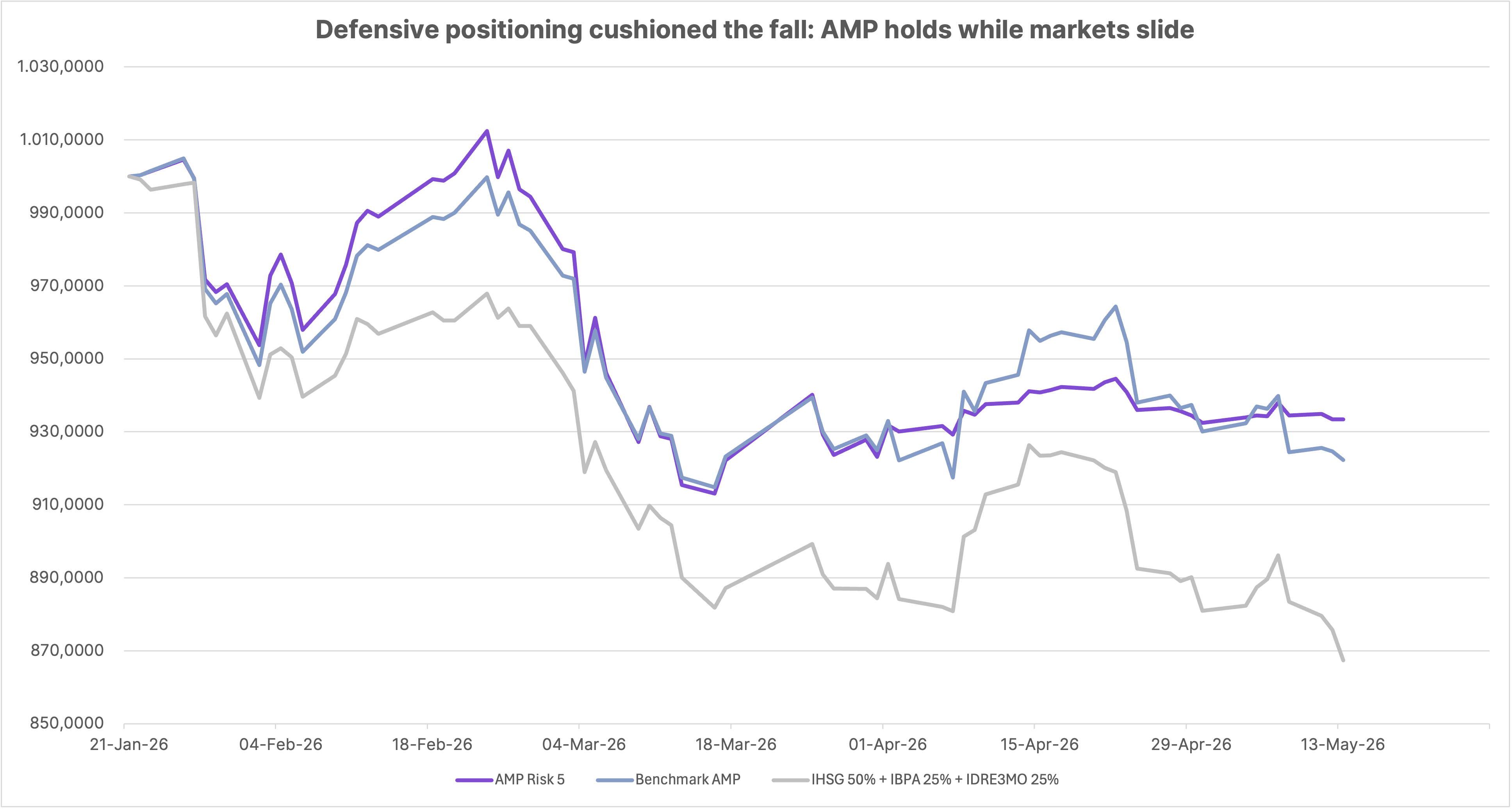

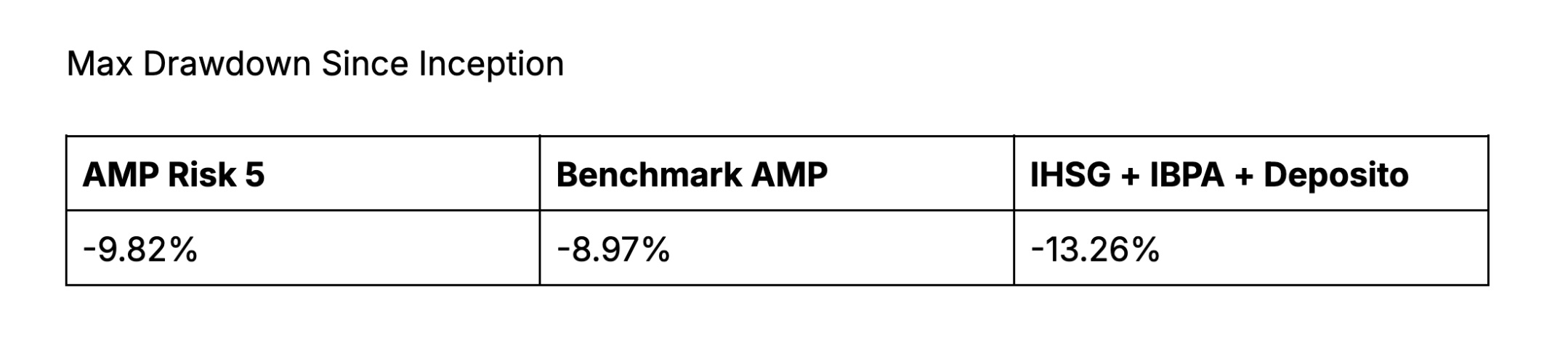

Actively managed portfolios

We had already positioned defensively heading into May, with equity allocation at 12% and balanced positions of 44% each in cash and bond funds. That posture was designed precisely for moments like this: to preserve capital while retaining the flexibility to redeploy risk as conditions stabilise. AMP is doing what it was built to do, so that you do not have to time anything yourself.

The market this month has been an uncomfortable reminder that investing in any single country, even one with Indonesia’s long-term potential, demands patience for the periods when the story gets complicated and the headlines get loud. Historically, those tend to be exactly the moments worth holding through.

As always, we are here if you want to talk through your positioning.