The Floor Holds: Indonesia Avoids Frontier Downgrade

Indonesia retains its MSCI emerging market status. Here's what changed, what didn't, and how we're positioning through continued uncertainty ahead of the November 2026 review.

The MSCI 2026 Market Classification Review has concluded. For Indonesia, the outcome is clear: MSCI has confirmed Indonesia's emerging market status.

This was, in our view, the expected outcome. Indonesian authorities took meaningful steps to address MSCI’s concerns around market accessibility — notably through improvements in shareholder granularity disclosure and the introduction of a high concentration list. These weren’t cosmetic changes; they were the specific reforms MSCI had flagged, and they appear to have been sufficient to prevent an immediate downgrade.

That said, the MSCI statement makes clear that announcements alone aren’t enough. What matters now is consistent implementation and sustained effect. MSCI will continue to assess the scope, consistency, and effectiveness of these measures — and if sufficient progress isn’t evident by the November 2026 Index Review, reclassification to Frontier Markets remains on the table.

What the Market Said

The JCI closed at approximately Rp 5,900 on June 24, down 3.37% on the day, with turnover of around Rp 13 trillion. Month-to-date, the index is down 2.82%, with foreign investors recording net outflows of Rp 20.6 trillion over the period.

The reaction reflects two things at once: the relief of avoiding an immediate downgrade was already partially priced in, while the caveats around implementation and the November deadline introduced uncertainty the market is still absorbing. This isn’t a collapse in fundamentals. It’s a market reacting to an ambiguous outcome.

Indonesia’s economy expanded at 5.61% in Q1 2026 — a strong headline number, but one driven largely by government spending rather than private consumption or investment. Growth of that composition is less self-sustaining, and as fiscal consolidation progresses, the tailwind from public expenditure will likely moderate. We’re bullish on the valuation; we’re also clear-eyed about the quality of the growth underpinning it. We continue to favour staying invested and selectively adding on weakness, with that in mind.

How We’re Thinking About This

Equities

The JCI is now trading at a forward P/E of 14.23x, roughly two standard deviations below its historical mean — valuation levels last seen during COVID. At these prices, we remain bullish. Historically, entry points at these levels have rewarded patient investors.

Fixed Income

Indonesia’s 10-year government bond yield is currently at 7.21%. At this level, fixed income presents a compelling entry point for investors already holding rupiah assets. We continue to recommend increasing exposure and extending duration where appropriate.

Currency

The rupiah has weakened to approximately Rp 18,100 against the US dollar, and the pass-through to businesses and households is real. There are early encouraging signs — the rupiah had recovered to around Rp 17,800 in recent sessions — but we remain cautious. The durability of any IDR recovery hinges on fiscal credibility, and we’re watching government spending commitments closely. Follow-through on APBN consolidation remains the key signal for sustained stabilisation.

Our Overall Position: Stay Invested

These past few weeks have been testing. The index has reached COVID-era valuations, the currency has weakened to multi-year lows, and the MSCI review has extended the uncertainty to November. None of that is trivial.

But at current valuations, the risk premium on Indonesian assets looks attractive. The reforms that kept Indonesia in the EM index are real, even if their sustained implementation remains the open question. Historically, the periods when the story is most complicated and the numbers look worst have tended to be precisely the moments worth holding through. We’ll continue to monitor developments ahead of the November window and update you as things evolve.

How to Position Through This

For investors staying invested in Indonesian markets: Actively Managed Portfolio (AMP)

Indonesia’s market can be illiquid at times, which means foreign flows tend to have an outsized impact on prices, creating sharp moves that can feel disconnected from fundamentals. AMP was built for exactly this environment — adjusting your allocation between equities, bonds, and money market instruments each month based on market conditions. At current levels, where both equities and fixed income present compelling entry points, we think this is a good time to enter or add. AMP provides the structure to do so in a disciplined way, without having to navigate the volatility alone. The strategy has historically protected capital through episodes like the 2013 Taper Tantrum and COVID-19 while still participating in recoveries.

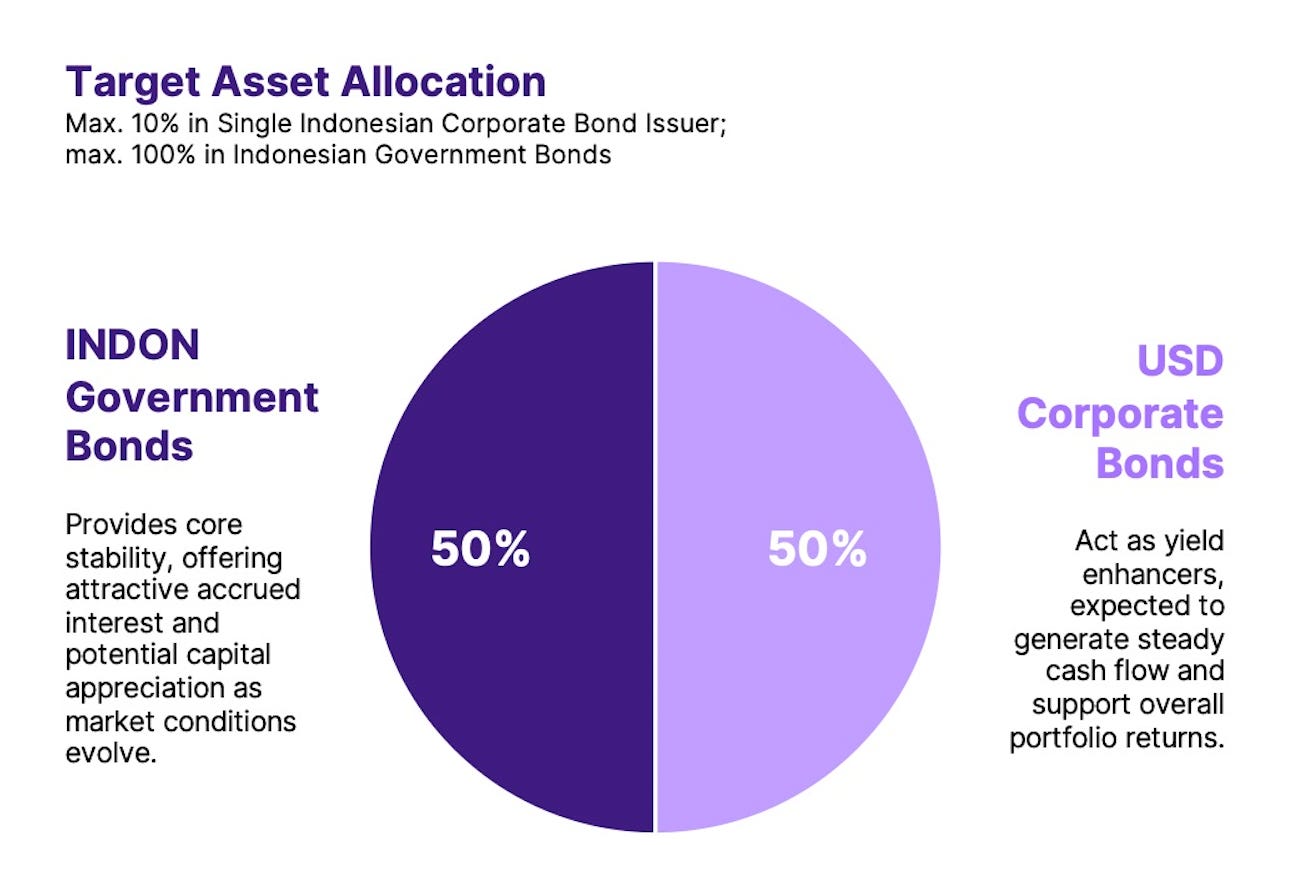

For investors looking to diversify away from IDR: Dollar Bond Fund (DBF)

For clients concerned about rupiah weakness, the Dollar Bond Fund offers USD exposure through a mix of USD-denominated Indonesian government and corporate bonds — quality fixed income instruments, outside of rupiah risk. Over the past 20 years, the IDR has depreciated at approximately 4% per year against the USD, a persistent structural headwind for unhedged rupiah assets. DBF exists for clients who want to grow their wealth in USD terms without fully stepping away from Indonesia. Contact us here to learn more.