Rupiah at a Crossroads: Cyclical Pressure or Structural Shift?

What's driving Rupiah weakness, how foreign investors actually see Indonesia, what the Rupiah is actually worth, and how investors should position their portfolios.

Dear Clients,

Rupiah weakness has been dominating headlines lately, with USD/IDR breaking above the 17,000 level. The question a lot of people have been asking is: is this just temporary, or are we looking at a new normal?

To answer this question, our Investment Team recently published a research piece covering key topics such as structural drivers behind Rupiah’s weakness, how foreign investors actually see Indonesia, what the Rupiah is actually worth, and how investors should position their portfolios. Below is a quick breakdown of the key points. For the full analysis, you can access the complete report here.

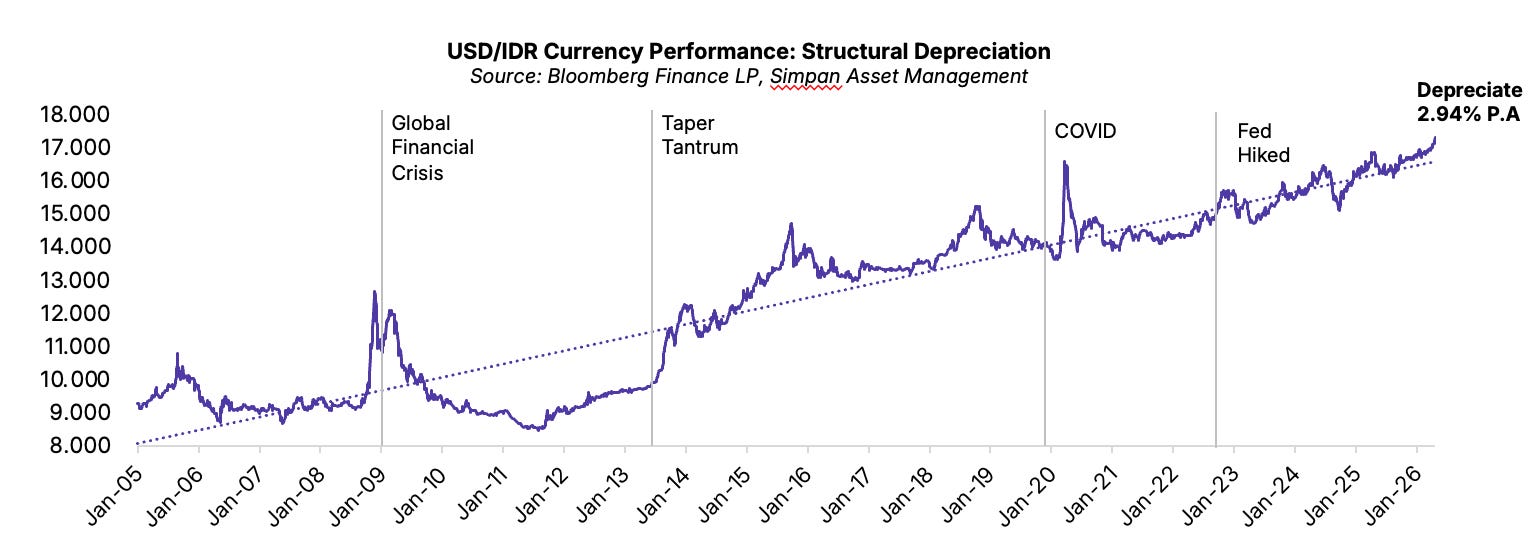

Rupiah Depreciation Isn’t New

As shown in the chart below, the Rupiah has weakened by ~85% against the USD since 2005, translating to an annualized depreciation rate of ~2.9%. Two structural factors drive this weakness: inflation differentials between the U.S. and Indonesia, and a persistent current account deficit.

Since 2022, depreciation has accelerated to ~3.5% annually, reflecting the unwind of the global carry trade—the mechanism that supported the Rupiah throughout the 2010s.

What Do Foreign Investors Actually See?

Equities: Currency Drag Erodes Returns

The Jakarta Composite Index (JCI) has delivered ~9.6% annual returns in IDR terms over the past two decades. However, that’s not the number that foreign investors see. When the returns are converted back into USD, currency depreciation has consistently eroded returns, making Indonesian equities far less attractive, thus making it difficult to retain foreign investors and capital.

Fixed Income: The Carry Trade Is Breaking

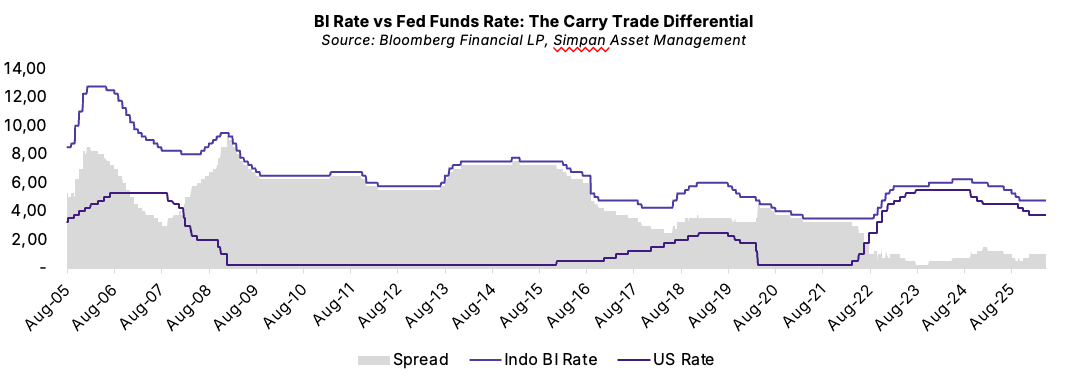

Indonesian government bonds (SBN) were historically the primary vehicle through which foreign investors engage with Indonesia. The “carry trade” phenomenon involves foreign investors borrowing cheaply in USD and using it to invest in higher-yielding IDR SBNs.

However, the “net carry”, what a US investor actually earns after costs, is far less attractive, shown in the table below. This explains why foreign SBN demand has seen a structural decline, even though gross yields have remained elevated.

Furthermore, the rate differential between the U.S. and Indonesia has narrowed in recent years, reducing the margin of safety for carry trades and making IDR assets less attractive relative to developed markets. At the same time, sovereign risk has increased, with Indonesia’s 10Y CDS (Credit Default Swap) around 136 bps — way above the 100 bps level that typically raises concern among global investors.

With credit ratings sitting near the lower end of investment grade (Baa2/BBB), there is limited buffer before a potential downgrade, further weighing on investor sentiment.

Foreign Flows: The Structural Exit

In recent years, foreign ownership in Indonesian equities and fixed income has declined significantly. Foreign ownership of JCI market capitalisation has declined from a peak of approximately 40% in 2013–2014 to around 18% by April 2026. In fixed income, ownership has collapsed from 38.5% in 2019 to 12.6% in April 2026.

That being said, there is a contrarian implication. With foreign ownership already significantly reduced, the scope for further selling is more limited. Our view is that, once the Rupiah begins to stabilize, the upside from renewed inflows could be more meaningful. That being said, the next major directional move in foreign positioning is more likely to be inflows rather than continued outflows.

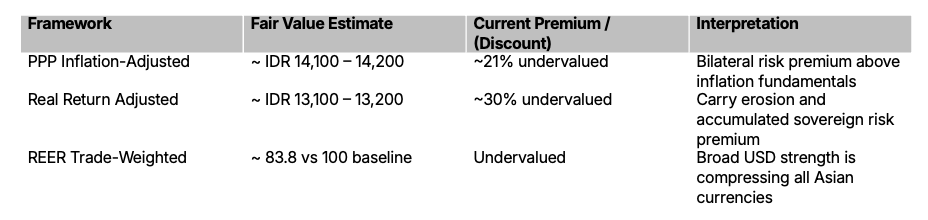

What is the Rupiah Actually Worth?

Our Investment Team conducted three valuation frameworks: Purchasing Power Parity (PPP), Real Return Adjusted, and Real Effective Exchange Rate. Through these three frameworks, we conclude that the Rupiah is undervalued. For a more detailed explanation of our valuation methodologies, click here to read our research paper.

This suggests that the current exchange rate level is not a fundamental equilibrium but rather a liquidity and risk-premium price, driven by factors that are at least partially cyclical and therefore potentially reversible.

What’s Needed to Stabilize the Rupiah?

We identified three key factors, outlined below:

1. Necessary Conditions: The Cyclical Pivot

The Rupiah is heavily influenced by external “global gravity,” meaning domestic policy alone cannot stabilize it. A durable floor depends on three shifts: a credible Fed easing cycle to restore rate differentials and weaken the USD, lower oil prices (ideally below $85/bbl) to ease fiscal and current account pressures, and stable FX reserves to maintain market confidence. Without improvement in these factors, structural pressure on the IDR is likely to persist.

2. Structural Catalysts: The Policy Shift

Cyclical improvements alone won’t stabilize the Rupiah; lasting strength requires shifting from a “trading proxy” to an investment-driven currency with steady USD inflows. This hinges on higher-quality FDI — particularly export-oriented manufacturing (à la Vietnam) rather than commodity-linked inflows — alongside deeper domestic demand for government bonds to reduce reliance on foreign capital. Additionally, expanding local currency settlement and de-dollarization efforts can gradually reduce structural USD demand. Together, these reforms would build a more resilient and self-sustaining foundation for the IDR.

3. The Credit Rating Overhang: Indonesia’s Biggest Tail Risk

A sovereign downgrade is the biggest tail risk for the Rupiah, as it would trigger forced selling across bonds and equities and overwhelm BI’s ability to stabilize the currency.Indonesia currently holds investment-grade ratings from all three major agencies: Baa2 from Moody’s (equivalent to BBB), BBB from S&P, and BBB from Fitch. But with negative outlooks, a cut toward BBB- or below could drive index exclusion, capital outflows, and higher borrowing costs. Key risks to watch are a widening fiscal deficit, rising debt levels, and weakening FX reserves. A shift from negative outlook to an actual downgrade would likely accelerate IDR depreciation.

Given the Recent Rupiah Weakness, What Should Investors Do?

Equities:

Maintain exposure to commodity linked and export oriented equities, especially companies that earn their revenue in USD (e.g. Indonesian coal, CPO, nickel producers). At the same time, be selective on import dependent sectors. Furthermore, watch the big-cap banks as a proxy for inflow; when foreign flows return, big caps are usually first.

Fixed Income:

Stay cautious. Favor short- to mid-duration SBNs and maintain higher cash buffers. Longer duration only becomes attractive once spreads stabilize and a Fed pivot is credible.

Bottom Line

To summarize, Rupiah weakness isn’t a mystery. It’s a result of years of inflation differentials, persistent current account deficits, and a steady withdrawal of foreign capital, leaving the currency on a structurally weaker path. Foreign investor behavior reinforces this: USD-based equity returns have been eroded by currency drags, while bond ownership has fallen to multi-decade lows as the carry trade becomes less attractive.

At the same time, valuation models suggest the Rupiah is meaningfully undervalued, suggesting that current levels are driven more by risk premium and global conditions than fundamentals. The key downside risk remains a potential credit rating downgrade, which could trigger forced outflows and further increase pressure on the currency.