Monthly Investor Update May 2026

Market events in May, how our funds performed, and our outlook ahead.

Dear Clients,

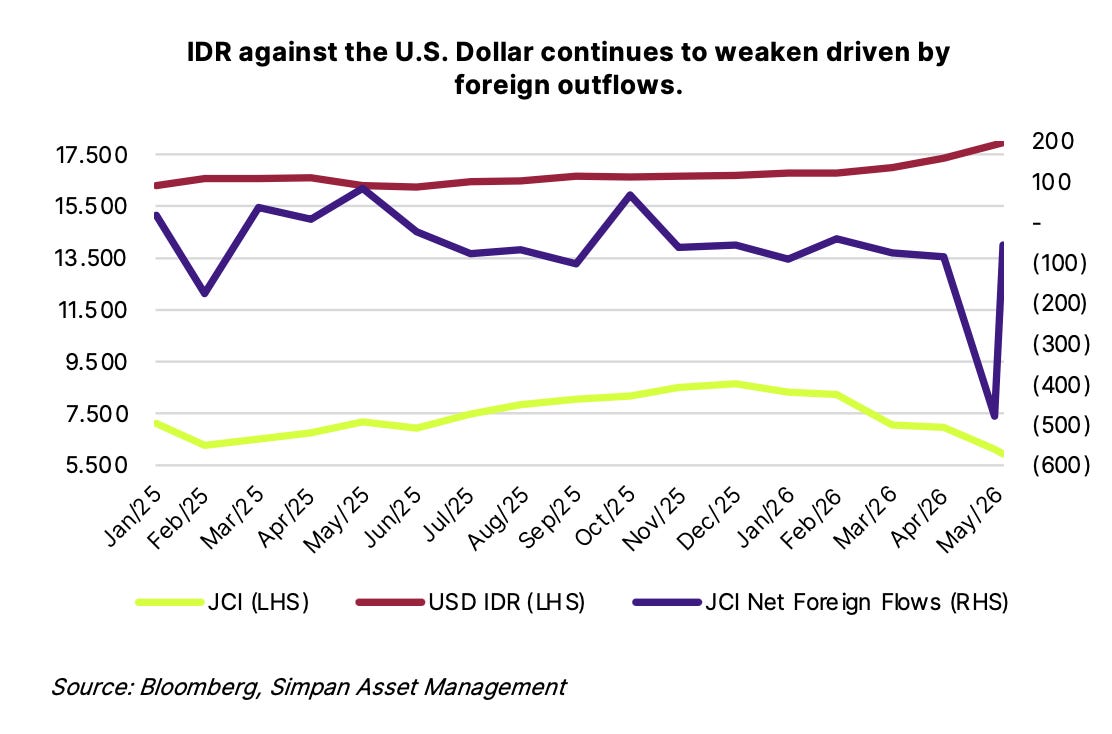

May was a difficult month for Indonesian markets. The IHSG fell 11.92%, a sharp deterioration from April’s -1.30%, driven by a combination of aggressive foreign selling, new government export regulations, and a Rupiah that broke through the 17,800 level against the US Dollar. Through our May Monthly Investor Update, we outline what happened, how our funds performed, and how we are thinking about what comes next.

May Market Highlights

1. The JCI Fell 11.92% — Its Worst Monthly Performance in Recent Memory

Indonesian equity markets came under severe pressure in May, with monthly losses accelerating sharply from the -1.30% recorded in April. The selloff was broad-based, driven by a confluence of domestic policy uncertainty and sustained foreign outflows tied to the MSCI Indonesia rebalancing. Foreign investors recorded net outflows of approximately IDR 19.44 trillion from the MSCI Indonesia universe, with selling concentrated heavily in momentum-driven stocks and conglomerate names. The JCI is now at year-to-date lows, though from a valuation standpoint this begins to open up selective entry opportunities for disciplined investors.

2. New Government Export Regulations Added to Policy Uncertainty

One of the more significant domestic developments in May was the introduction of new export regulations for selected commodities. Under these rules, export activities can now only be conducted by government-appointed authorities, effectively reducing private sector participation. This added a layer of regulatory uncertainty on top of already fragile market sentiment, and directly impacted the performance of commodity-linked equities.

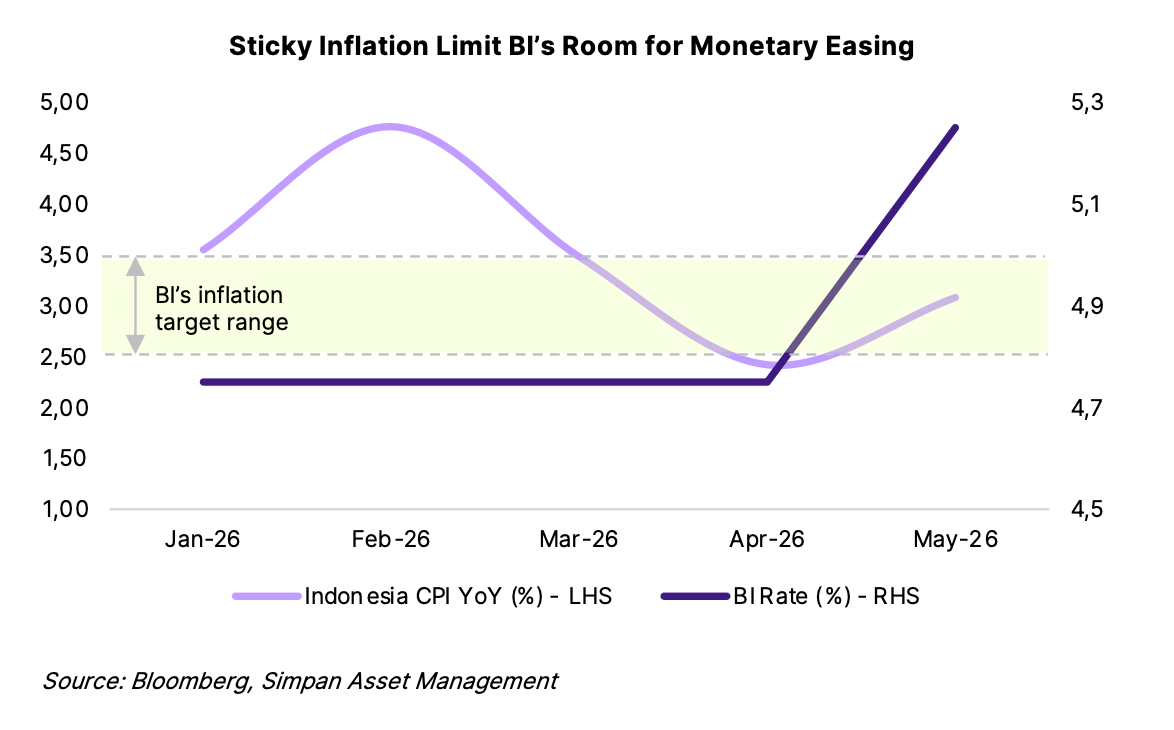

3. Bank Indonesia Raised the BI-Rate by 50bps — More Than Markets Expected

Sustained foreign outflows put additional pressure on the Rupiah, pushing USD/IDR through the ~17,800 level. In response, Bank Indonesia raised the BI-Rate by 50 basis points, exceeding market expectations of a 25bps hike. The move was primarily aimed at stabilizing the currency amid continued US Dollar strength. Beyond the rate decision, BI also intervened in the fixed income market through purchases of mid-to-long tenor government bonds and implemented capital flow management measures to support domestic bond yields and reduce the risk of further capital flight.

How Did Simpan’s Funds Perform?

All funds under our management, except Simpan Bond Fund and Simpan Cash Fund, underperformed their respective benchmarks in May. This outcome was broadly in line with market conditions — the sharp equity correction and sustained foreign outflows weighed on risk assets across the board, and no equity-oriented strategy was fully insulated.

That said, our AMP portfolios held up better than their benchmarks at every risk level. Risk 2 through 5 portfolios outperformed due to their relatively lower equity exposure going into the month, a positioning we had maintained from April’s rebalancing. Risk 1 portfolios experienced a modest drag from longer duration positioning in our bond holdings, though the impact was contained. Our fixed income funds fared well — the Simpan Bond Fund returned +0.43% against a benchmark of +0.29%, as government bond yields trended lower over the month.

Market Outlook & Portfolio Positioning

Our outlook for June is neutral on Indonesian equities. Much of the negative sentiment from May appears to have been priced in, and the MSCI rebalancing — which was a major source of selling pressure — has now run its course. That said, markets remain cautious, and we are not yet at a point where we would describe conditions as clearly improving.

A few key events in June will shape the path ahead. S&P Global Ratings is due to deliver its sovereign outlook decision for Indonesia, and MSCI will conduct its market accessibility assessment during the month. Both carry the potential to meaningfully influence sentiment in either direction. The USD/IDR level and concerns around Indonesia’s fiscal sustainability also continue to weigh on investor confidence.

Against this backdrop, we have made a measured shift in portfolio positioning. We are gradually increasing equity exposure across AMP portfolios, moving away from the fully defensive stance of recent months, and doing so selectively — focusing on companies with strong fundamentals, resilient balance sheets, and clear earnings visibility that we believe are better placed to weather continued volatility.

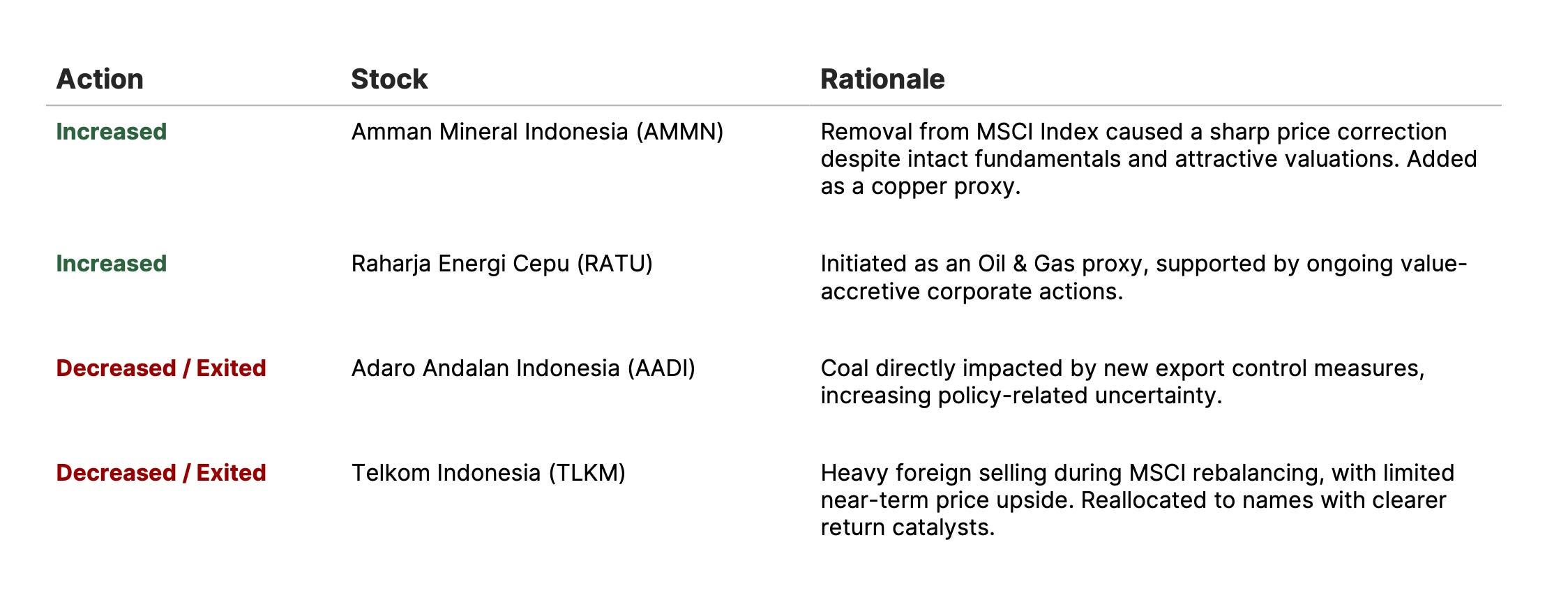

Below is a summary of some of the key trades we made in May:

Equities — Key Trades

Fixed Income — Key Trades

In Fixed Income, we maintained a cautious approach to duration with an average portfolio duration of 5.70 years, slightly above the benchmark’s 5.30 years. We are actively monitoring opportunities to selectively extend duration, particularly at the shorter end of the yield curve where risk-reward dynamics have become more attractive. Geopolitical developments in the Middle East remain a key area of focus given their potential flow-through to oil prices, the Rupiah, and global liquidity conditions including petrodollar flows.

We will continue to monitor developments closely and remain fully committed to managing your investments with the same care and diligence as ever. As always, thank you for your continued trust.