Monthly Investor Update February 2026

Market events in February, how our funds performed, and our outlook ahead.

Dear Clients,

February was a volatile month across equities, with the Jakarta Composite Index (JCI) closing out lower by -1.08% MoM. Through our February Monthly Investor Update, we discuss market highlights, how our funds performed, our outlook ahead, and how we’re positioning portfolios.

First, let’s briefly recap what happened across markets in February:

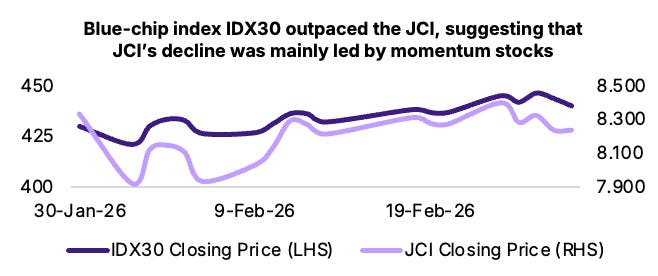

The JCI rebounded in initial weeks but market sentiment weakened towards month-end, due to rising geopolitical tensions in the Middle East, continued Rupiah weakness, and lack of clarity around MSCI-related issues.

Despite broader market weakness, the blue-chip index IDX30 closed out higher by ~+2%, suggesting that weakness in the JCI was primarily driven by momentum stocks.

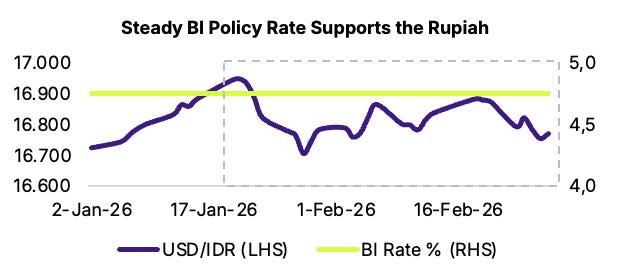

BI kept rates unchanged at 4.75%, primarily to support the Rupiah which has seen ongoing weakness (edged closer to ~17,000 USD/IDR), driven by heightened global financial uncertainty.

Moody’s downgraded Indonesia’s credit outlook from “Stable” to “Negative”, largely due to growing warnings about policy uncertainty around Danantara & fiscal policy direction. The news caused a wave of selling across equities and bonds, with 5Y and 10Y yields spiking.

Amid volatility, how did our funds perform?

Despite broader market weakness, all our funds delivered positive performance in February, although our Equity Fund and Bond Fund underperformed benchmarks.

Although the JCI corrected, our equity portfolios gained, as we realized profits opportunistically in names that have seen a sharp run up, particularly within the nickel sector. All our AMP portfolios also saw gains, though risk 2 - 5 portfolios slightly underperformed benchmarks.

For a closer look at the specific stocks we bought or sold, read our February Monthly Investor Update.

In Fixed Income, 10Y and 5Y yields traded higher, with foreign ownership stable at roughly 13% of total issuance.

Simpan’s Views

With the ongoing geopolitical tensions, we expect markets to remain volatile in the near-term. We also expect uncertainties surrounding MSCI policy changes to further weigh on investor sentiment. Furthermore, rising oil prices following the closure of the Strait of Hormuz pose inflationary risks for Indonesia, a net oil importer, which could widen the fiscal deficit and place additional pressure on the Rupiah.

Amid ongoing equity volatility, we are adopting a “risk-off” stance, focusing on increasing exposure to commodity-linked stocks such as gold, coal, and oil & gas, given their earnings resilience and effectiveness as hedges against macro and market volatility.

Though we expect a bearish outlook for March, the recent correction has made equity valuations more compelling, allowing us to gradually increase allocation to equities for some of our AMP portfolios (risk 3 – 5). However, we remain cautious and are not positioning aggressively yet, as we continue to monitor developments closely while the situation evolves.

In Fixed Income, we plan to gradually extend duration further, but are also staying cautious in the near-term due to inflationary pressure risks from higher oil prices, possible yield shocks in the government bond market driven by widening fiscal deficit concerns, and the persistence of elevated interest rates.

Thank you for your continued trust.