Monthly Investor Update April 2026

Market events in April, how our funds performed, and our outlook ahead.

Dear Clients,

Indonesian markets continued to see volatility in April, as geopolitical tensions, persistently elevated oil prices, and Rupiah weakness continued to dampen investor sentiment. Through our April Monthly Investor Update, we outline market highlights, Simpan’s funds’ performance, our outlook ahead, and how we’re positioning portfolios.

April Market Highlights

1. Jakarta Composite Index (JCI) Traded Volatile, Closing Out Lower By -1.30% in April

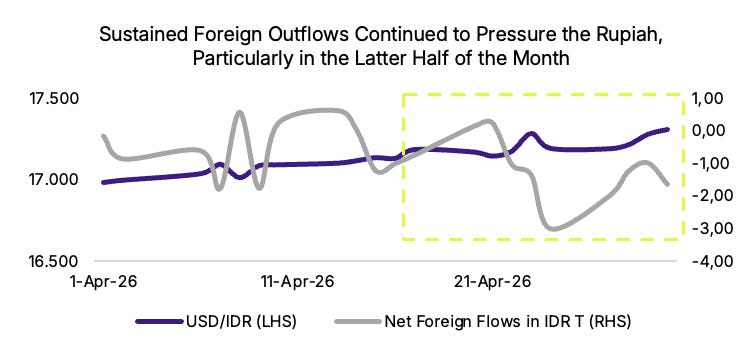

The JCI rebounded in the first half of April but came under pressure in the latter half, ultimately closing the month down by -1.30%. Elevated energy prices continued to raise concerns over Indonesia’s inflation and fiscal outlook, weighing on investor sentiment and triggering broad-based weakness across equities. Foreign investors remained net sellers, recording outflows of ~IDR 17.72T, largely concentrated in major banking stocks such as BBCA, BBRI, and BMRI. Persistent capital outflows also added pressure on the Rupiah, with USD/IDR breaching above the ~17,300 level during the month.

2. Both BI and The Fed Kept Rates Unchanged

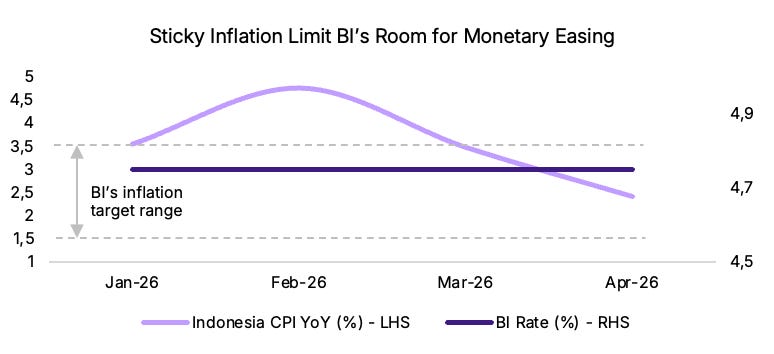

Amid heightened uncertainty, the Fed maintained its benchmark rate, adopting a “wait-and-see” approach as it balanced persistent inflationary pressures against a resilient but gradually moderating labour market. Similarly, BI kept rates unchanged to prioritize Rupiah stability. Indonesia’s March CPI rose to 3.8% YoY, above BI’s target range of 1.5% – 3.5%, limiting the central bank’s room for monetary easing in the near term.

How Did Simpan’s Funds Perform?

Despite heightened market volatility, all of our funds delivered positive returns during the month, with all funds outperforming their respective benchmarks except for our Bond Fund. In particular, our equity-oriented portfolios outperformed the JCI, supported by our prior positioning in commodity-linked names.

Our AMP portfolios also generated positive returns and outperformed benchmarks. Performance in Risk 1 portfolios was primarily driven by gains in bond holdings, while returns in Risk 2–5 portfolios were mainly supported by our equity allocations.

Market Outlook & Portfolio Positioning

Our outlook for May remains bearish, particularly due to geopolitical tensions that still persist. Elevated energy prices continue to raise concerns over inflationary pressures and Indonesia’s fiscal position. In addition, we expect the upcoming MSCI index rebalancing and continued Rupiah weakness to sustain foreign outflows, which could further pressure domestic markets.

Given the fragile near-term risk sentiment, we are maintaining a defensive investment stance. In equities, our strategy remains focused on companies with strong earnings visibility and resilient fundamentals. We remain constructive on commodities, supported by elevated energy prices, resilient demand, and their role as a hedge against macroeconomic uncertainty and inflation.

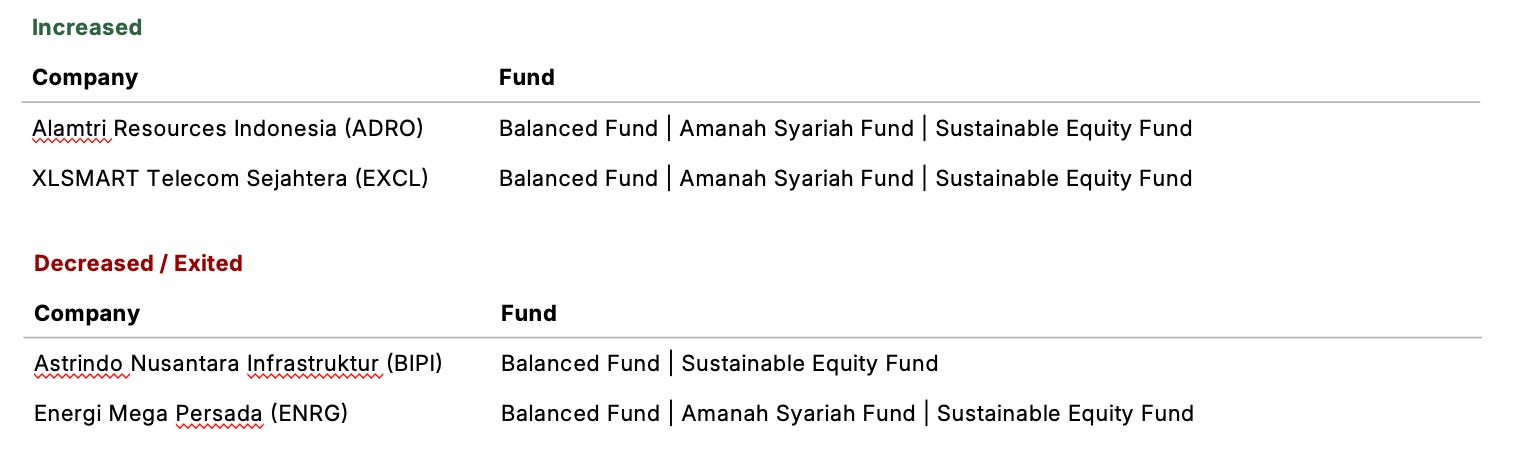

Below are some of the stocks we bought and sold in April:

In Fixed Income, we maintain a cautious stance on duration, while monitoring opportunities to extend duration as yields become more attractive. Given geopolitical risks, we are also closely tracking implications for global liquidity, including petrodollar flows and potential policy responses in Indonesia, especially around the fiscal deficit and inflation.

Across AMP portfolios, we are keeping portfolio allocation unchanged. Within Risk 2 –5 portfolios, the relatively lower equity exposure and higher allocation to cash and fixed income instruments provide flexibility to increase equity positions opportunistically once there are clearer signs of market stabilization, such as easing geopolitical tensions, a strengthening Rupiah, or a return of foreign inflows.

We continue to monitor developments closely and remain committed to managing your investments with the same dedication and care as ever. We thank you for your continued trust.