Monthly Investor Update March 2026

Market events in March, how our funds performed, and our outlook ahead.

Dear Clients,

In March, escalating geopolitical tensions between the US/Israel and Iran weighed heavily on investor sentiment, triggering a broad-based sell-off across both equities and bonds. Through our March Monthly Investor Update, we outline what happened, how our funds performed, and our outlook ahead.

March Market Highlights

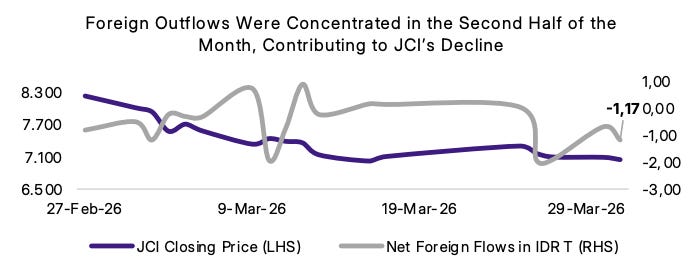

JCI Saw Significant Pressure, Declining -14.2% MoM

In addition to geopolitical tensions, Rupiah weakness, elevated oil prices, and MSCI-related uncertainty reinforced a risk-off environment. As a result, the JCI declined -14.2% MoM, with the blue-chip index IDX30 down around -12%.

Foreign investors recorded net outflows of ~IDR 9T, with selling concentrated in banking names, specifically BBCA, BBRI, BBNI.

Global & Domestic Bond Market Under Pressure As Well

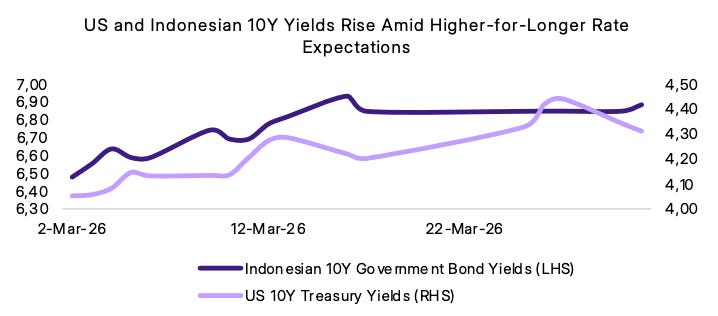

Elevated oil prices and inflation concerns drove a repricing of interest rate expectations, triggering a sell-off in the bond market both globally and domestically. As a result, US 10Y Treasury yields rose ~28 bps, while Indonesian 10Y Government Bond yields rose ~41 bps.

The Fed and BI Held Rates Steady

The Fed maintained rates at 3.5 – 3.75%, adopting a wait-and-see stance amid geopolitical uncertainty, higher than expected inflation readings, and mixed signs on the labor market. BI also held rates at 4.75%, prioritizing Rupiah stability and inflation control. However, they signaled room for rate cuts, provided the Rupiah stabilizes and inflation is controlled.

Simpan’s Funds Performance

Amid broader market weakness, almost all our funds posted declines and underperformed benchmarks, with the exception of our money market funds. However, our equity-oriented portfolios still outperformed the JCI, supported by our prior positioning in commodity-linked sectors.

AMP portfolios also declined, with Risk 1 impacted by bond exposure, while Risk 2–5 reflected broad-based equity weakness.

Simpan’s Market Outlook

We maintain a bearish outlook for April, driven by a “triple threat” of geopolitical tensions, currency instability, and MSCI rebalancing risks. Elevated oil prices above $100/bbl are expected to sustain inflationary pressures and pressure the Rupiah, while recent sovereign credit outlook downgrades have further weighed on foreign sentiment.

We expect continued volatility ahead of the MSCI review, with potential weight reductions in Indonesian equities posing risks of passive outflows. A sustained shift back to risk-on conditions would likely require clear de-escalation in the Middle East (specifically, a ceasefire that brings Brent below $85/bbl), or meaningful Rupiah stabilization.

Portfolio Positioning

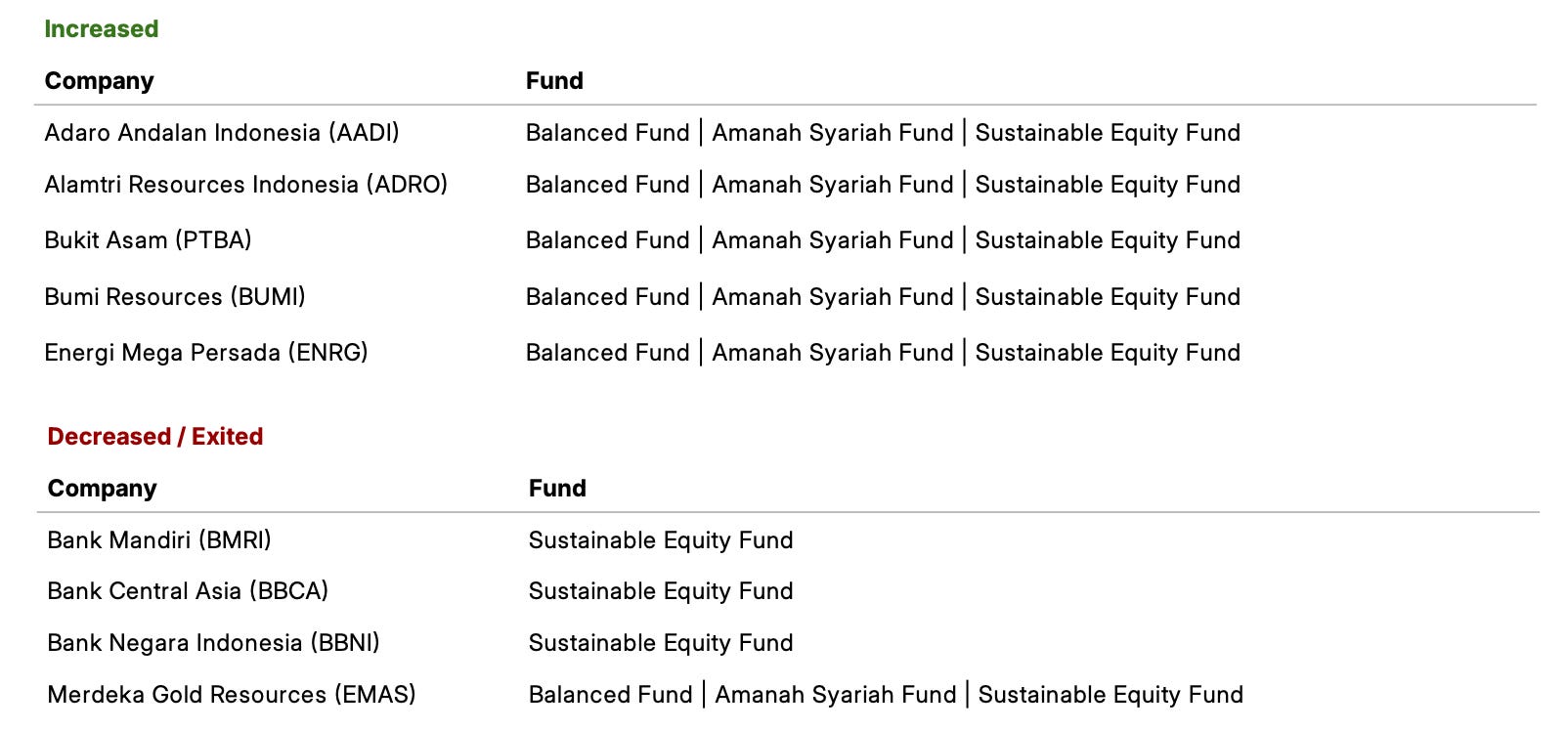

Against this backdrop, we maintain a defensive and cautious positioning across both equities and fixed income. In equities, we are holding disciplined cash buffers, while our portfolio is heavily weighted towards commodity-linked sectors and inflation-resistant energy names. Specifically, we increased exposure to the coal sector, as well as a tactical allocation to select oil & gas names.

Below are some of the stocks we bought and sold.

In fixed income, we maintained our duration positioning. While yields have begun to ease, we are closely monitoring risks arising from developments in the Middle East, particularly through their direct impact on oil prices, bond yields, and the Rupiah.

Across AMP portfolios, we have reduced equity exposure in Risk 2–5 portfolios to limit downside risk and volatility, and instead increased allocation towards money market and bonds. In Risk 1 portfolios, we reduced allocation to bonds and increased allocation to money market, to preserve portfolio stability and reduce sensitivity to interest rate movements.

Amidst this challenging and uncertain environment, we continue to monitor developments closely and remain committed to managing your investments with the same dedication and care as ever. We thank you for your continued trust.