How The U.S. Attack on Venezuela Impacted Markets

Key Developments in Geopolitics, Commodities, and Market Performance

Geopolitical Developments and Market Implications

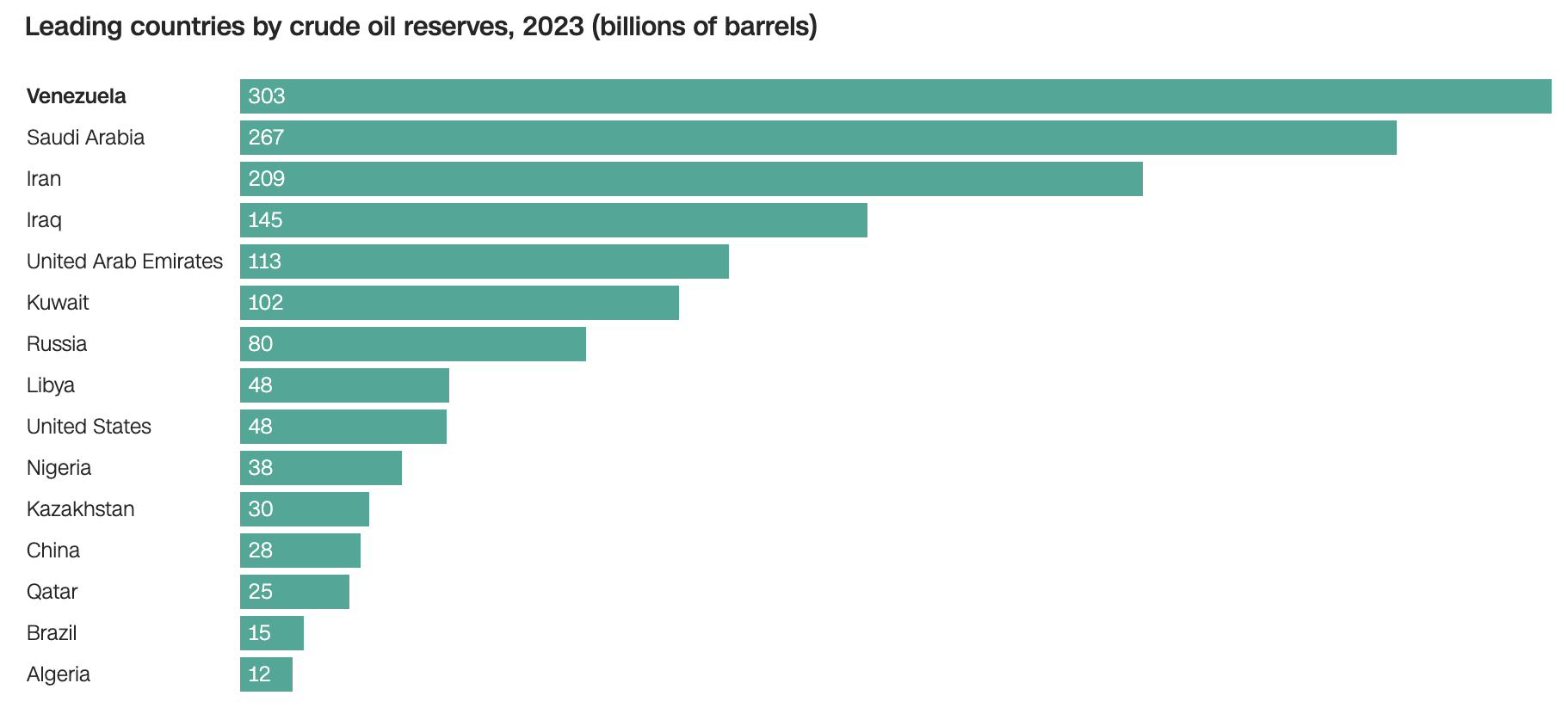

Over the past weekend, geopolitical tensions surrounding Venezuela came into focus, following the U.S. military attacks in Venezuela and the capture of President Nicolas Maduro. President Donald Trump also stated that the U.S. plans to seek control over Venezuela’s substantial oil reserves and encourage American companies to invest heavily in refining the country’s deteriorated oil infrastructure. For context, Venezuela has about a fifth of the world’s proven crude oil reserves.

Source: CNN Business

President Trump noted that U.S. oil companies could invest billions of dollars to restore Venezuela’s oil sector and revive its energy infrastructure. If his plan moves forward, there are several key implications to monitor. U.S. control over Venezuelan oil would likely disrupt global oil and energy markets, with the potential for sharp increases in both WTI and Brent prices.

For Indonesia, as a net oil importer, sustained higher oil prices would translate into higher import costs. Combined with a strengthening U.S. dollar if they take control of the oil reserves, this could lead to increased inflation in the country, particularly through higher raw material and energy prices.

Market & Commodities Reaction

In commodities, U.S. crude oil (WTI) declined to below USD $57 per barrel on Monday morning, their lowest levels since 2021, but soon stabilized, gaining roughly +2% on Monday and closing at USD $58.2 per barrel. Typically, when there is geopolitical tension with oil producing countries, oil prices tend to spike immediately. This time, we did not see an immediate price reaction, as the U.S.’ plan to take control of Venezuela has the potential to bring more oil and natural gas supply to the market, raising concerns around oversupply risks.

U.S. equity markets traded modestly higher. The S&P 500 gained +0.67%, while the Nasdaq Composite rose +0.79%. The three largest oil-service companies: Halliburton Company (NYSE: HAL), SLB Limited (NYSE: SLB), and Baker Hughes (NASDAQ: BKR) all jumped roughly +5%. Investor optimism increased as these global oil giants are well positioned to benefit from expanded U.S. access to the world’s largest crude reserves.

Domestically, we did not see an immediate impact on Indonesian markets. The JCI closed out higher by +1.27% on Monday, although gains were again driven by momentum stocks, not blue-chips. Foreign investors remained net sellers of IDR 9.98B, with supply absorbed by domestic investors. The U.S. Dollar Index (DXY) strengthened modestly to 98.68. Amid rising uncertainty, investors rushed to safe-haven assets, with gold rising approximately +2.3% and silver gaining around +4.3%.

In this environment, demand for gold stands a chance to rise as geopolitical uncertainty intensifies. Rising tensions between the U.S. and China, coupled with increasing unpredictability in global policy direction, would support safe-haven demand. As a result, gold prices rose to a one-week high, up 2.7% to $4,444 an ounce.

De-globalization Risks

In our view, President Trump’s move risks opening a broader geopolitical Pandora’s box, materially escalating tensions across regions and asset classes. Any forced removal of Venezuela’s sitting president would likely generate meaningful spillover effects across global energy markets, maritime trade routes, and geopolitical alliances.

Disruptions could arise not only from operational shutdowns or sanctions but also from higher shipping costs, insurance premiums, and rerouting of trade flows.

This situation also poses significant risks to U.S.-China relations. Venezuela is an important oil supplier to China and a critical component of Beijing’s broader South American strategy, both in terms of energy security and overseas investments. A regime change driven by the U.S. would likely impair China’s access to Venezuelan oil assets and undermine the value of its existing loans and infrastructure investments. This could provoke strategic pushback from China and Russia, further polarizing global alliances and complicating the geopolitical landscape.

From a longer-term perspective, if the U.S. were to gain influence over Venezuelan oil production and facilitate a recovery in output, global oil supply could structurally increase. This would be disinflationary for energy prices and reinforce U.S. dominance in global energy markets, including a stronger role for the petrodollar system. However, such an outcome would likely follow a prolonged period of instability and elevated risk, rather than an immediate normalization.

Simpan’s View

As an asset management firm, our role is to filter short-term noise and remain focused on long-term outcomes. During periods of heightened uncertainty, it’s important to stay cautious. Therefore, we continue to recommend maintaining exposure to our Cash Fund.

Equities

While the JCI continues to trade near record highs, we anticipate a pickup in market volatility and do not rule out a near-term pullback over the coming days or weeks. That said, we remain constructive on Indonesian equities, as the direct impact from recent global developments appears manageable and domestic fundamentals remain supportive. However, we are mindful of tail-end risks that could trigger abrupt sentiment shifts and lead to sharp, short-term corrections.

Against this backdrop, we are maintaining a defensive stance across our equity funds. Recent price action in several holdings has provided opportunities to gradually derisk and lock in gains. Maintaining a healthy cash position enhances portfolio flexibility, allowing us to respond decisively should more attractive entry points emerge or as geopolitical tensions begin to ease. This approach enables us to protect capital in the near term while preserving the ability to reallocate efficiently when risk-reward dynamics improve.

Fixed-Income

In Fixed Income, 10Y yields remain steady at around 6.1%. At current levels, we do not view this as an attractive entry point for bonds. Overall, we favor a defensive positioning with higher cash allocations. Staying invested in our Cash Fund enables investors to earn incremental returns while preserving capital, ensuring funds remain productive rather than idle as markets navigate uncertainty.

In the short term, softer oil prices are supportive for Indonesia’s domestic fixed-income market, as lower energy costs ease imported inflation and improve the trade balance, giving Bank Indonesia greater room to maintain a stable or accommodative policy stance.

On the fiscal side, reduced fuel subsidy pressures improve government financing dynamics and may lessen issuance pressure, supporting bond valuations, particularly in the intermediate to long tenors. While weaker oil prices could still trigger short-term volatility if they signal slowing global demand, the overall domestic fixed-income backdrop remains constructive.